Flexible payments have become a defining feature of modern commerce. What started as a convenience for smaller consumer purchases has evolved into a strategic growth lever for coaches, creators, and digital businesses selling education, expertise, and premium products and services online.

But as price points rise and audiences globalize, we asked ourselves the question: Is there a better way?

Today, we’re excited to introduce ThrivePay Installments, a new, credit card-linked installment solution designed specifically for high-value digital commerce, global audiences, and merchants who want to offer flexible payments without taking on repayment risk or encouraging new consumer debt.

This article serves as both a product launch announcement and a comprehensive guide to how ThrivePay Installments works, where it fits alongside BNPL, and why it represents a fundamental shift in how installment payments should work for modern digital businesses.

Want a deeper dive before reading further? Watch our ‘ThrivePay Installments Explained’ webinar, including Q&A detailing exactly how it works, with examples.

The new reality of digital commerce

Creators, educators, coaches, and entrepreneurs are no longer just selling $29 ebooks or $99 mini-courses as their primary revenue stream. Instead, we’re seeing rapid growth in:

- Professional certifications and career training (especially in AI)

- Advanced coaching and mentorship programs

- Health, wellness, and transformation journeys

- Memberships, masterminds, and premium communities

- High-touch digital services delivered globally

- A mixture of physical and digital products complementing each other in one funnel

These products often sell for $1,000 to $10,000+, sometimes significantly more.

The game-changing role BNPL has played – and where it fits perfectly

- Ticket sizes are relatively low

- Purchases are impulse-driven

- Transactions are local or region-specific

- Products are consumer-oriented and physical

Where BNPL needs a rethink

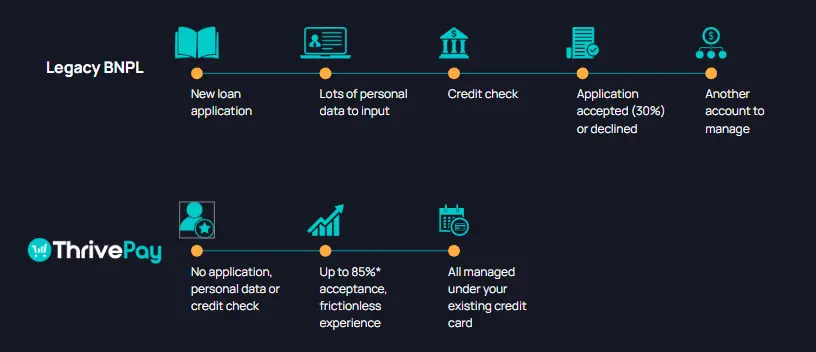

- Approval rates often hover around 40% due to underwriting and credit checks

- Ticket caps typically fall around $1,500-$2,000

- Checkout friction increases due to redirects, forms, and third-party apps

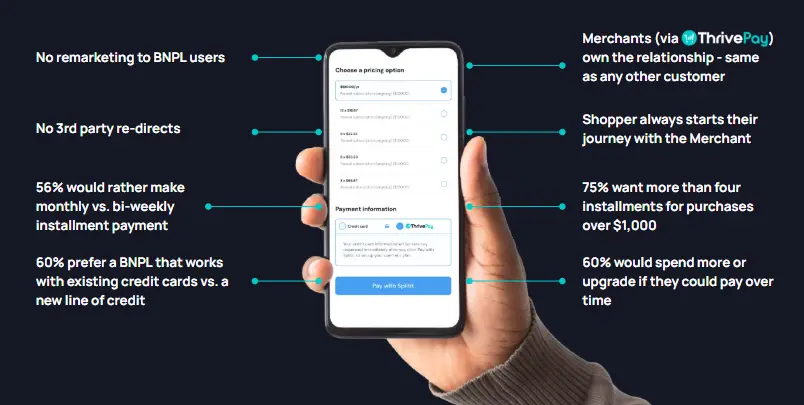

- Customer relationships are partially owned by the BNPL provider

Real-world evidence: the model needed to evolve

Introducing ThrivePay Installments

- The full purchase amount is authorized on the customer’s card

- The customer repays the balance over 3, 6, or (in some cases) 12 months

- The merchant is paid upfront

From the customer’s perspective, the experience feels familiar and seamless. From the merchant’s perspective, it fundamentally changes the risk and cash-flow equation.

How ThrivePay Installments works (step by step)

- Customer selects ThrivePay Installments at checkout

- Full amount is pre-authorized on their existing credit card

- No loan application, no new account, no credit check

- Payments are scheduled over the chosen term

- Merchant receives funds upfront, rather than waiting months

Because the authorization relies on limits already approved by card issuers, approval rates are significantly higher (80-85%) versus loan-based BNPL models (~40%).

Why ThrivePay Installments performs better

1) Dramatically higher approval rates

Traditional BNPL requires underwriting. ThrivePay does not.

Because authorization is handled by card networks and issuers, ThrivePay delivers 80-85%+ approval rates, compared to ~40% for many BNPL flows.

That difference alone can transform checkout performance for high-ticket products.

2) Much higher order values

ThrivePay Installments can support transactions up to $65,000+, depending on available credit limits.

BNPL is often capped around $2,000.

This allows merchants to:

- Sell higher tiers

- Bundle services and add-ons

- Confidently price premium offerings

3) Global reach without fragmentation

ThrivePay Installments can then tap into the following markets:

- U.S.

- Canada

- United Kingdom

- European Union

- Australia

Because it operates within existing card payment frameworks, ThrivePay is far easier to expand internationally than loan-based BNPL solutions, which often require country-specific underwriting and regulation.

4) Upfront merchant payout

With ThrivePay Installments:

- The merchant is paid upfront

- Repayment is handled at the card level

- Cash flow becomes predictable

This is particularly important for businesses with delivery costs, staff, or fulfillment tied to the initial purchase.

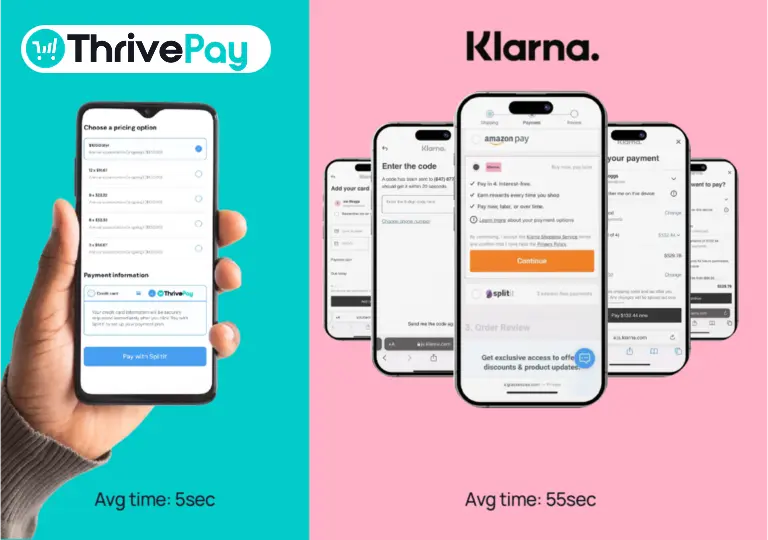

5) Zero checkout friction

ThrivePay Installments requires:

- No application

- No personal data entry

- No third-party redirect

- No new account to manage

The result is a faster checkout, a cleaner experience, and higher completion rates.

Unlocking an underutilized pool of purchasing power

- Consumers hold approximately $4.1 trillion in authorized credit card limits

- Roughly $3.3 trillion of that remains unused

- Around 75% of U.S. consumers have FICO scores above 650

These are established, financially stable buyers – often the exact audience purchasing high-value digital products.

ThrivePay Installments is designed to unlock this purchasing power responsibly, without encouraging consumers to take on new debt.

Ethical by design: payments, not debt

- It does not originate new loans

- It does not create new credit accounts

- It does not impact credit scores

- It does not encourage debt stacking

Customers can only spend within limits already set by their card issuer.

The result is a payment experience that feels like paying smarter, not borrowing more.

Regulatory resilience and long-term stability

BNPL providers are increasingly subject to:

- Affordability checks

- Reporting requirements

- Capital constraints

- Jurisdiction-specific compliance

Because ThrivePay operates as a payment method, not a lending product, it carries lower regulatory complexity and is better positioned for long-term global availability.

Where ThrivePay fits – and where BNPL still thrives

BNPL works best for:

- Low-ticket purchases

- Local consumer retail

- Off-card financing

- Impulse-driven buying

ThrivePay Installments excels for:

- High-intent buyers

- Larger purchases

- Global audiences

- Digital-first businesses

- Premium education and services

Merchants can – and often should – offer both, using the right tool for the right scenario.

Use cases by business type

- Course Creators & Educators: Sell advanced certifications, multi-course bundles, and career programs without price-anchoring lows.

- Coaches & Consultants: Offer high-ticket programs while removing upfront friction and protecting cashflow.

- Health & Wellness Brands: Enable customers to commit to longer transformation journeys with predictable payments.

- Memberships & Masterminds: Reduce churn risk while still offering flexible access to premium communities.

A complete payments stack on ThriveCart

- ThrivePay Installments: Card-linked installments with upfront payout

- Legacy BNPL: Including Affirm, Klarna, and Afterpay

- Split Pay: Merchant-managed payment plans

- Limited Subscription Rebills: Fixed-term recurring revenue

- Pay As You Like: Flexible or donation-based pricing

- One-time digital and physical product payments

- Subscription digital and physical product payments

- Crypto payments

All hosted within ThriveCart, or they can be fully embedded. All no-code. All merchant-owned. QR scanner options for all.

Frequently asked questions (FAQ)

It is initially offered to customers in the U.S., Canada, the UK, the EU, and Australia. Later, it will become available to merchants in any region where ThriveCart operates

What installment terms are available?

Three and six months initially, with 12-month terms available on a case-by-case basis.

When do merchants get paid?

Payouts are currently made every 15 days, with plans to shorten this over time.

Is there a reserve?

Yes. A 15% rolling reserve over 180 days applies.

Who is eligible?

Merchants with a charge back rate under 0.25% and a refund rate under 5%. Subect to T&Cs.

Who handles chargebacks and refunds?

Chargebacks and refunds remain the merchant’s responsibility and are deducted from reserves or future payouts if necessary.

Can I still offer BNPL?

Yes. ThriveCart allows you to offer ThrivePay Installments and BNPL side by side, with rules to control visibility.

The next era of flexible payments

ThrivePay Installments represents the next step in that evolution, enabling merchants to sell higher-value products to global audiences, with less friction, less risk, and more control.

Flexible payments aren’t going away. But the way they’re delivered is changing.

And this is what the future looks like..